Genuine Parts (NYSE: GPC) has more than doubled the total return of the S&P 500 index since the turn of the century. However, since 2022, shares of the automotive and industrial parts leader have declined 23% as inflation ballooned and spending from manufacturers tightened.

So, has Genuine Parts — a Dividend King with 68 consecutive years of dividend increases — finally lost its way? Or is this dip in share price due to shorter-term cyclicality, providing investors with a long-term opportunity?

Here’s why I’m thinking the latter.

GPC: A global leader in automotive and industrial parts

Home to 9,900 automotive parts stores and 720 industrial parts distribution centers, GPC operates in North America, Europe, and Australasia through two business segments:

-

Automotive group (62% of sales, 50% of operating profit): Powered by its National Automotive Parts Association (NAPA) brand, this automotive replacement parts segment generates 63% of its sales in North America. What differentiates this group from its peers is that 80% of its sales come from professional repair technicians, whereas this figure is only 53% for O’Reilly Automotive and much lower for AutoZone. Focusing on the pro side of the auto community, GPC maintains a sticky base of sales from major accounts, government customers, companies with fleets of vehicles, and installers. Better yet, GPC collects 25% of its revenue from Europe, a geography that is untouched by O’Reilly or AutoZone.

-

Industrial group (38% of sales, 50% of operating profit): A leading industrial parts distributor, Motion Industries sells to a wide array of end markets ranging from equipment, food products, and mining to automotive, chemical, and logistics. Currently, roughly three-quarters of its sales come from products like bearings, power transmission, industrial, safety supplies, hydraulics, pneumatics, and miscellaneous products.

Typically, GPC’s two business segments, automotive and industrial, combine for a perfect yin and yang operationally, with one group picking up the other’s slack in more cyclical times. However, this has not been the case over the last year.

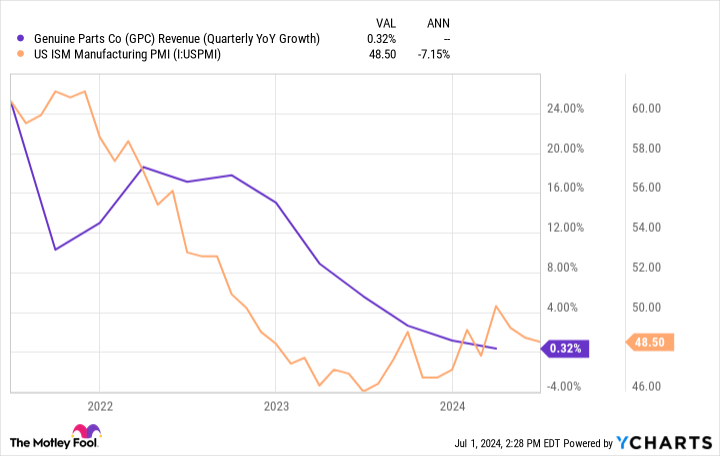

Combining for flat sales growth overall in the first quarter of 2024, GPC’s automotive and industrial segments struggled to lap 7% and 12% same-store sales growth from last year. As worrying as these results seem, though, the next few quarters could turn brighter for GPC as the Purchasing Manager’s Index (PMI) has begun improving over the last year.

Measuring the health of the manufacturing industry — a key portion of the broader industrial sector — a PMI below 50 shows that manufacturers’ activity is contracting rather than expanding. While the PMI still sits below 50, it has begun moving higher, reinforcing GPC’s claims that its industrial unit’s growth should restart in the second half of the year.

Meanwhile, though the automotive unit’s sales have also lagged, the company is expanding full speed ahead into Europe and Australasia, opening 112 and 22 new stores in each geography, respectively.

Investors should welcome these expansion plans with open arms, thanks to GPC’s robust return on invested capital (ROIC) figures from the past decade.

Robust profitability powers this Dividend King forward

Averaging a ROIC of 14% over the last decade (which included negative abnormalities from the pandemic), GPC has proven capable of driving outsize profitability compared to its debt and equity. In simple terms, as the company expands — whether through building new stores or bringing in bolt-on acquisitions — it does an excellent job wringing profits out of its new locations as soon as possible.

What makes these capabilities really exciting is that GPC has spent around $270 million annually in acquisitions since 2015. Combined with its persistently high ROIC, this highlights a long track record of successfully integrating new businesses.

Thanks to its long-standing ability to reinvest in its operations, GPC has become a Dividend King. This title is reserved only for S&P 500 stocks that have increased their dividend payments consecutively for 50 years or more — and the companies on this list read like a who’s who of blue chip businesses.

Incredibly enough, despite growing its dividend for 68 straight years, GPC has a payout ratio of 42%. This means that the company only has to use 42% of its net income to fund its 2.9% dividend yield.

Still easily funding its dividend payments, there is plenty of room for further increases for years, if not decades, down the road.

Why buy GPC now?

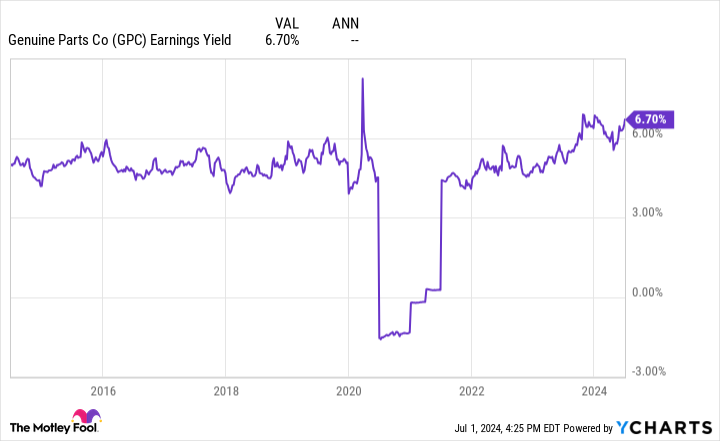

With an earnings yield of 6.7% (which is essentially the inverse of a company’s price-to-earnings (P/E) ratio, so higher is better), GPC is trading near a once-in-a-decade valuation.

Not only is this a higher earnings yield than its own traditional levels, but it is markedly higher than the S&P 500’s average of 4%.

Last but not least, if we use a reverse discounted cash flow model with GPC, we find that the company only needs to grow by 5% annually to justify its current share price, assuming a market-matching 10% discount rate and 3% terminal rate. Growing sales by 7% and 5% over the last five and 10 years, this mark could prove to be quite achievable.

While macroeconomic cyclicality appears to have finally caught the company for a brief moment, GPC should be poised to restart its growth over the coming quarters and looks all but certain to continue raising its dividend for years to come.

Should you invest $1,000 in Genuine Parts right now?

Before you buy stock in Genuine Parts, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Genuine Parts wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $786,046!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 2, 2024

Josh Kohn-Lindquist has positions in AutoZone and O’Reilly Automotive. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Magnificent Dividend King Down 23% to Buy Right Now Near a Once-in-a-Decade Valuation was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel

Surge, And Is It Justified?")