Investing in stocks near their 52-week highs doesn’t fit the classic “buy low, sell high” mantra. However, William O’Neil, the author of How to Make Money in Stocks, argues that this is precisely where investors should begin their search for a new top-tier business to buy.

With the best stocks tending to continue setting new highs year after year, these top performers act as a stocked pond of sorts to go fishing in as we look for our next market-beating investment.

One such company is smart mobility solutions provider Verra Mobility (NASDAQ: VRRM), whose share price has steadily risen from $6 in March 2020 to roughly $30 today.

Providing an end-to-end suite of solutions ranging from automated toll road transponders and payments to road safety cameras for school buses, bus lanes, and work zones, Verra is early in its growth story but already creating abundant cash flows. Here’s why I believe the company is an excellent candidate to prove William O’Neil right over the long haul.

What does Verra Mobility do?

Hitting the public markets in 2018, Verra Mobility is a leading provider of smart mobility technologies that help make transportation safer, more efficient, and more connected. To give some concrete examples of what Verra does, let’s analyze its three business segments:

-

Commercial Services (46% of sales): Verra’s largest unit consists of toll management, violations management, and titling and registration servicing for rental car companies (RACs), direct fleets, and fleet management companies (FMCs). The company sets up toll transponders for its customers’ fleets, offering cashless toll processing while managing payments for any violations that may occur. Verra has long-standing relationships with the three largest RACs and the five biggest FMCs in the United States.

-

Government Solutions (44% of sales): This segment provides road safety cameras to state and local governments across the U.S., Canada, and Australia. By detecting violations for red lights, speed limits, school bus stop-arms, work zones, and bus lanes, Verra’s end-to-end solutions aim to provide safety to cities’ “high-value” areas such as school zones or heavily trafficked streets. If a violation occurs, the company can process the citation in-house for its customers.

-

Parking Solutions (10% of sales): The company’s smallest unit serves over 2,000 customers across the healthcare, municipal, and enterprise markets and is the leader in parking solutions for universities in the U.S. Processing more than 162 million transactions in 2023, Verra’s parking solutions manage access, usage and citation payments, permit issuance, event parking, and various back-office operations.

What makes Verra Mobility an attractive stock is the high switching costs it has with its large fleet, government, and university customers. Once customers sign up for the company’s mobility solutions, they tend to stick around, as evidenced by Verra’s impressive 95% customer renewal rate. This stable sales base creates a moat around Verra’s business that makes it harder for incumbent companies to try to disrupt.

Adding further intrigue to the company’s investment thesis is the fact that 96% of Verra’s revenue comes from recurring services sales. These recurring sales, paired with the company’s strong renewal rates, create a solid foundation of sticky sales that shouldn’t fluctuate much from year to year.

Verra Mobility’s numerous routes to growth

Over the last three years, Verra has doubled its revenue, including a 9% increase in its most recent quarter. Powered by its high renewal rates and high cross-sell potential across its products — especially its government solutions segment — the company is positioned to continue inching sales higher for years to come.

However, there is more to Verra’s growth story than cross-selling opportunities. First, its commercial services segment is expanding into Europe, where cashless tolls are much less common. Currently, 67% of tolls in the U.S. are cashless, but in France, for example, this figure is only 5%, leaving a long potential growth runway in Europe for Verra.

Second, the government solutions segment should continue to see steady growth, as California, Washington, Florida, Connecticut, Pennsylvania, and Colorado all recently passed automated enforcement legislation. This development clears the path for Verra to supply the states with its safety cameras for school buses and school zones.

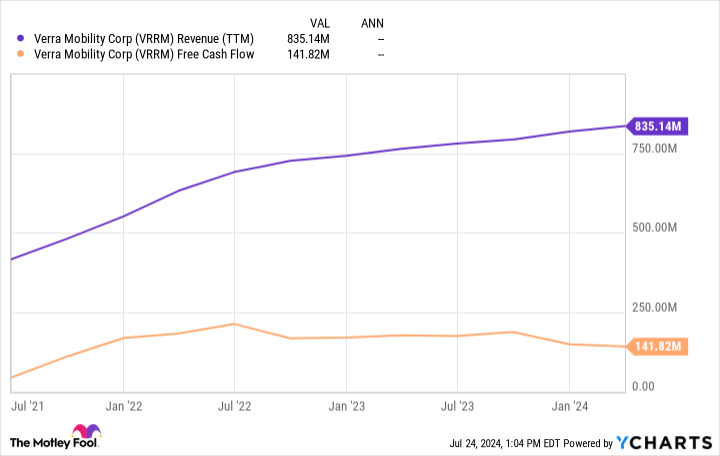

Robust free cash flow generation

As promising as Verra’s growth story is, the company’s history of strong free cash flow (FCF) creation is equally as impressive. Powered by an incredible 95% gross profit margin, the company converts its sales into FCF at a high rate.

While Verra’s FCF has dipped slightly over the last two years as the company expands its toll operations internationally and grows the sales team for its government solutions, it still maintains a healthy 17% margin. Thanks to these high margins, the company is easily capable of handling its $1 billion in debt while also funding new buyback programs and monitoring potential acquisitions.

With management expecting somewhere around $160 million in adjusted FCF in 2024, Verra trades at 32 times FCF. Although this is slightly above the market’s average, Verra Mobility’s sticky sales base, long growth runway, and impressive margin profile make it worthy of this slight premium.

Ultimately, Verra Mobility’s unique operations could prove O’Neil’s “winners keep winning” mantra correct over the long haul, making it a promising candidate for dollar-cost-averaging buys from investors in 2024.

Should you invest $1,000 in Verra Mobility right now?

Before you buy stock in Verra Mobility, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Verra Mobility wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Josh Kohn-Lindquist has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 Top Growth Stock Up 119% Since 2023 to Buy and Hold Forever was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel