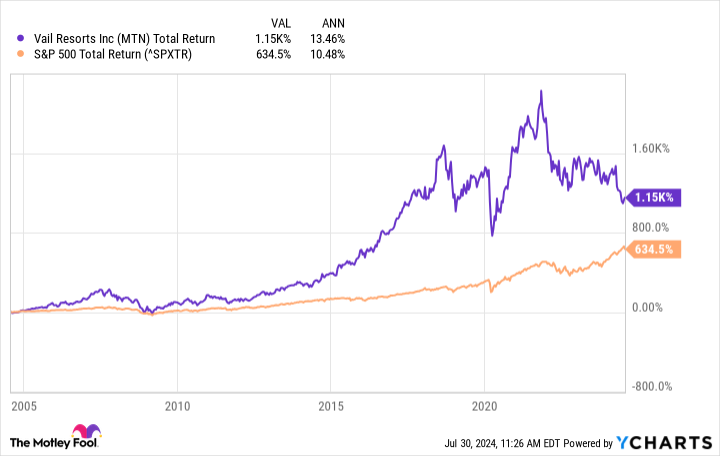

Battling a trio of challenges, including weaker consumer confidence, less snowfall at its North American ski resorts, and tough comparables after a post-COVID resurgence, Vail Resorts (NYSE: MTN) has seen its shares decline 50% since 2021.

While Vail is the largest global ski resort with 42 locations across North America, Australia, and Europe, it is still subject to the cyclical nature of its industry — and currently, most of these somewhat random factors are working against it.

However, thanks to the company’s leadership position, its wide moat, and the market’s harsh reaction to its stock, Vail Resorts could prove to be a magnificent dividend stock trading at a once-in-a-decade valuation. Here’s what makes it so intriguing right now.

An industry leader with a wide moat

Home to 37 ski resorts in North America — including the top three and five of the top 10 most visited annually — Vail Resorts dominates the ski resort industry on its home continent. Similarly, the company also operates three of the top five most visited resorts in Australia, rounding out Vail’s portfolio of popular skiing destinations.

While working from this position of power as the industry’s leader is an advantage in and of itself, the company further benefits from the fact that no new resort of scale has been developed in the last 40 years. In simplest terms, there are only so many good mountains available for ski resorts, and Vail has already staked its claim on the most popular ones.

This combination of Vail’s irreplaceable mountain resorts and its size and scale gives the company a wide moat around its operations. Generally speaking, businesses with one or more powerful types of moats like these are able to deliver long-lasting periods of success. Proving this notion to a certain degree, Vail has delivered total returns nearly double that of the S&P 500 index over the last two decades despite its recent 50% pullback.

However, just because the company already has a leadership position in its niche, don’t consider it a stodgy value stock. Purchasing its second European resort, Crans-Montana, for $107 million this year, Vail continued its expansion into the world’s largest ski market. Home to nearly three times the number of ski visits as North America, Europe could prove to be the next chapter of Vail’s growth story as the company takes a measured approach to expanding in the region.

Vail is skiing by 2024’s challenges

Despite facing a trio of cyclical challenges, Vail managed to grow earnings before interest, taxes, depreciation, and amortization (EBITDA), earnings per share, and free cash flow (FCF) by 11%, 17%, and 28%, respectively, in its all-important third quarter. These results occurred despite the company’s western North American resorts receiving 28% less snowfall this year, helping to spur an 8% drop in total skier visits during the quarter.

This persistent profitability and FCF generation during challenging operating conditions is a testament to the power of Vail’s growing and non-refundable subscription model of selling passes to its members. Now home to 2.4 million loyal subscribers, the company generates nearly three-quarters of its visits from pre-committed pass holders.

These pass holders ski three times as many days as non-subscribers who buy lift tickets. This tidbit is crucial as it provides Vail with more opportunities to sell its ancillary offerings, such as lessons, dining, and rental equipment, to skiers.

Now intent on disrupting its own rental supplies business, Vail is launching its ski equipment subscription, My Epic Gear. Testing very favorably at select resorts, My Epic Gear should lower the annualized cost of ski equipment for both owners and renters. Leveraging Vail’s vast equipment supply chain and the insights gleaned from its database of 25 million guests, Vail will cost-effectively provide skiers with the newest and most popular gear.

Why Buy Vail Resorts now?

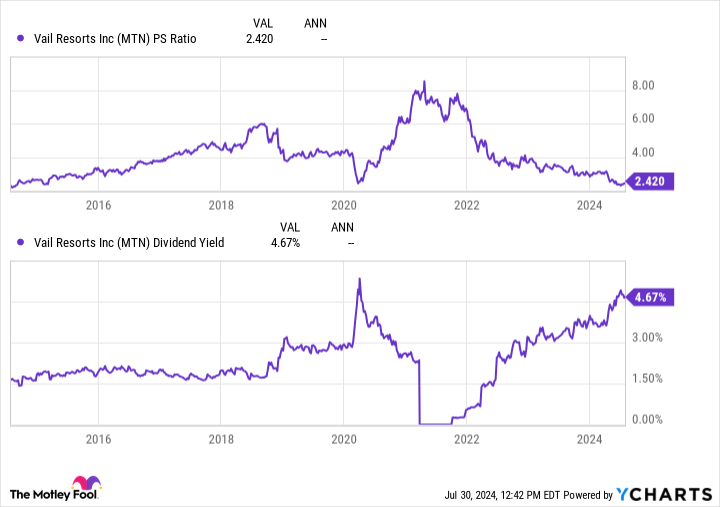

Currently, Vail’s price-to-sales (P/S) ratio is at its lowest level of the past decade.

Simultaneously, its 4.7% dividend yield is the highest it has ever been, outside of a brief moment in March 2020. Thanks to this combination of factors, Vail could prove to be a once-in-a-decade opportunity at today’s prices.

To put this P/S ratio of 2.4 in perspective, let’s assume that Vail is able to return its FCF margin to its historical average of 15%. Should this occur, the company would only be trading at 16 times FCF — a deep discount to market averages.

Furthermore, despite paying this hefty dividend, Vail only uses 83% of its FCF to make these payments. While this doesn’t leave a ton of room for future increases until its FCF margins return to normal, it shows that the dividend shouldn’t be at risk of getting cut anytime soon, either.

Ultimately, Vail Resorts’ leadership position in its niche and its wide moat should continue to help the company ride out the current down cycle, making it a magnificent dividend stock to buy at today’s once-in-a-decade valuation.

Should you invest $1,000 in Vail Resorts right now?

Before you buy stock in Vail Resorts, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Vail Resorts wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $657,306!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 29, 2024

Josh Kohn-Lindquist has positions in Vail Resorts. The Motley Fool has positions in and recommends Vail Resorts. The Motley Fool has a disclosure policy.

A Once-in-a-Decade Opportunity: 1 Magnificent Dividend Stock Down 50% to Buy Now and Hold Forever was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel