With 62 consecutive years of dividend raises, Coca-Cola is one of the safest and most consistent Dividend Kings. Its high yield, track record, and recession-resistant business model make Coke the embodiment of a blue chip dividend stock.

However, there are plenty of other reliable dividend stocks. Union Pacific (NYSE: UNP) is one of North America’s largest railroads, with a particular focus on the western two-thirds of the U.S. Over the past year, it paid $3.17 billion in dividends.

With its shares down 7% year to date, here’s why Union Pacific is a quality dividend stock worth buying now.

Laying the groundwork for a good investment

Railroads have unique business models. Unlike trucks and ships, they operate their own infrastructure and tend to dominate a particular geography. Their cost-effectiveness makes them a preferred method for transporting goods on land.

Union Pacific operates in a geographic duopoly with BNSF, the railroad owned by Berkshire Hathaway. Growth is based less on competing with the other heavyweights and more on operational improvements, managing an effective workforce, safety, and the business cycle.

Railroads are cyclical and depend on industrial production, gross domestic product, housing starts, light-vehicle sales, consumer spending, natural gas prices, and other economic indicators. There is little railroads can do about ebbs and flows in demand, but they can manage their spending in a way that drives margin improvements without compromising the quality of their service. That means maintaining a competent workforce and the structural integrity of the rail network.

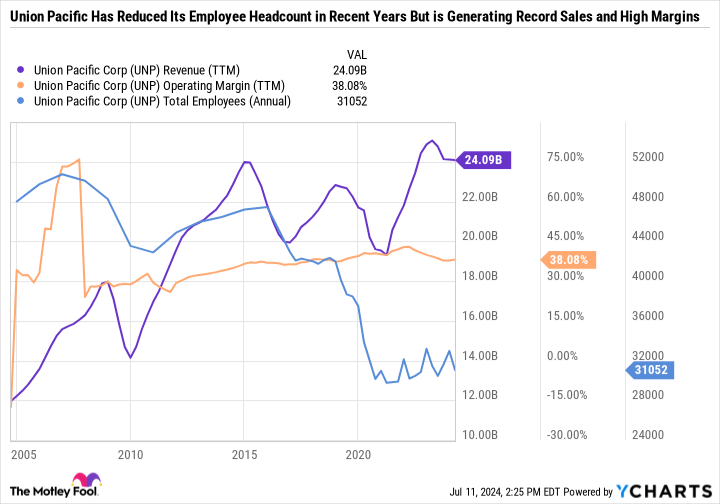

Doing more with less

Union Pacific stock has gone nowhere over the last three years. The pandemic significantly hurt supply chains and threw a wrench into demand forecasts.

In the years leading up to the pandemic, Union Pacific drastically reduced its workforce and focused on technology improvements to drive margin growth. The strategy mostly worked, but the railroad is still searching for a correct balance in the number of employees. Cutting staff can reduce expenses and improve profitability, but companies don’t want to reduce their headcount by so much that there’s little room to expand.

As the chart shows, Union Pacific’s margins have mostly stayed flat, and it has kept its head count down since the pre-pandemic reduction.

For now, the smaller footprint seems to be the right move. Cost reductions have helped compensate for a lack of volume growth. In its first-quarter 2024 earnings call, management said that it would love to see volume and revenue grow but that, in the meantime, it believes it is making the right moves on expenses and head count without affecting service.

Union Pacific has a diverse customer base

Instead of getting too caught up in the economic cycle, a better approach is to look at the growth drivers of the industries in which Union Pacific operates. In its June 2024 investor presentation, management outlined a breakdown of volume drivers for its first-quarter 2024 results. It measures freight revenue in three categories: bulk, industrial, and premium.

Revenue is fairly evenly split among bulk, industrial, and premium, each of which serves completely different end markets. Union Pacific isn’t just a bet on the growth of the overall U.S. economy, it is a bet on the major natural resource production regions in the western two-thirds of the U.S., which has a very different economy than the eastern third.

For example, Union Pacific is investing in expanded capacity and improved productivity in growing metropolitan regions in the Phoenix and Houston areas. Its Gateway to Mexico is instrumental in trade between the U.S. and Mexico.

Union Pacific’s dividend has room for improvement

Union Pacific has paid dividends for 125 consecutive years. However, it has only raised its dividend for 18 consecutive years, and some of those raises have been minor.

The best dividend-paying companies tend to raise their payout around the same time every year. But sometimes, companies will keep the dividend the same for several quarters so that the annual payout is technically higher and they can maintain their dividend streak.

Union Pacific has been doing this lately, which is definitely a red flag for future dividend growth. It raised its quarterly dividend from $1.18 per share in February 2022 to $1.30 per share in May 2022. The dividend has remained the same since then. But because of that slightly lower dividend payment in the beginning of 2022, the company paid $5.08 in dividends in 2022, and $5.20 in dividends in 2023.

As long as it raises its dividend at the end of this year, it will still achieve a higher annual payout — meaning Union Pacific can maintain its streak of consecutive yearly increases despite keeping the dividend flat for up to nine quarters in a row.

At a 2.3% yield, Union Pacific’s dividend is good but not great. However, it has been a particularly challenging operating environment, so it’s somewhat understandable that dividend raises have been unimpressive.

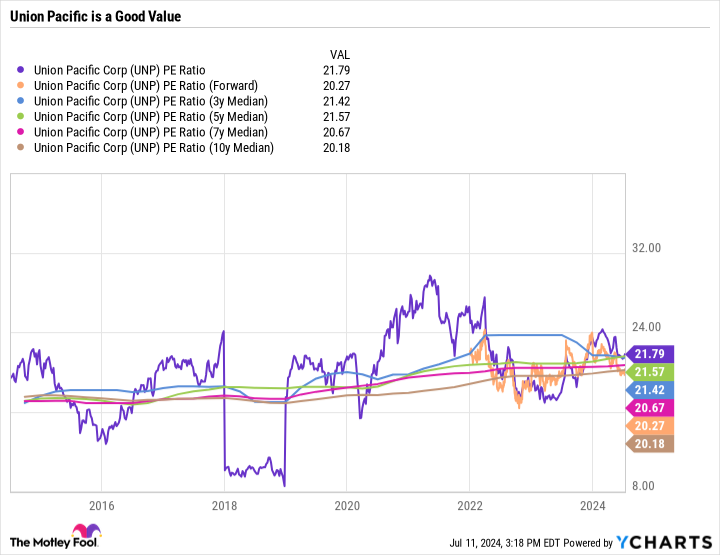

The bigger draw to the stock right now is the valuation. Its 21.8 price-to-earnings (P/E) ratio is close to its historical averages over the last 3 to 10 years.

The valuation seems reasonable for an industry-leading company. It’s also a notable discount to the 29.1 P/E of the S&P 500.

Hitch a ride on this balanced buy

Union Pacific is a good dividend stock to buy now, especially considering it differs considerably from traditional stodgy dividend stocks in the consumer staples sector like Coca-Cola. For an industrial, it does an excellent job of blending stability with potential upside from economic growth.

Railroads might see lower freight volumes during an economic downturn or recession, but there will still be demand for their services. So, although railroads are cyclical, they aren’t as boom or bust as an oil and gas producer that needs the oil price to be a certain level to break even.

Passive income investors looking to diversify their portfolios might want to consider Union Pacific.

Should you invest $1,000 in Union Pacific right now?

Before you buy stock in Union Pacific, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Union Pacific wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $791,929!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 15, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway and Union Pacific. The Motley Fool has a disclosure policy.

Coca-Cola Is a Rock-Solid Dividend King, but So Is This Dirt-Cheap Value Stock That Paid $3 Billion in Dividends Over the Past Year was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel