Less than a month from today, on Nov. 5, voters will head to the polls to determine which presidential candidate — current Vice President Kamala Harris or former President Donald Trump — will lead our country for the next four years.

Admittedly, not every decision made in the Oval Office or by our elected officials in Congress has bearing on Wall Street. However, the economic policies put into place by the incoming president and Congress do have the potential to affect corporate profits, and thus the stock market.

While there are potential advantages and drawbacks to the economic proposals of both candidates, the one plan that’s raising a lot of eyebrows on Wall Street is Harris’ call to raise the corporate tax rate by a third — from 21% to 28%.

Although the current U.S. corporate tax rate is at its lowest level since 1939, increasing it by 33% has the potential to set the stock market up for disaster for a very off-the-radar reason.

Stocks could plunge if Harris hikes the corporate tax rate — but not for the reason you might think

Kamala Harris’ plan to increase taxation on businesses stems from persistent and growing federal deficits.

With the exception of 1998 through 2001, the federal government has spent more than it has brought in via revenue every year since 1970. The national debt now sits around $35 trillion, with the annual cost to service this debt coming in at roughly $1.05 trillion as of August 2024, per the U.S. Department of the Treasury. This trajectory isn’t going to be sustainable over the long term.

Based on estimates from the Treasury Department, increasing the corporate tax rate by a third to 28% would lift federal tax revenue by a cumulative $1.35 trillion over the next decade.

However, increasing corporate taxes might have unintended and/or unforeseen consequences for Wall Street.

The logical expectation if the corporate tax rate climbs is that businesses will have less capital to put toward the meat and potatoes that makes them tick. Specifically, we’ll see a slower rate of new hiring, fewer acquisitions, and less in the way of capital spent on research and development. Hiring, acquisitions, and innovation are typically what grow the bottom line for businesses.

But there’s a less-obvious concern that can cause stocks to plunge if the corporate tax rate jumps by 33%. Less available capital to put to work for publicly traded companies might reduce or eliminate what’s been a key source of earnings growth in recent years: share buybacks.

For companies with steady or growing net income, share repurchases can boost earnings per share (EPS). As a company’s outstanding share count declines over time, its EPS should rise, thereby making it more fundamentally attractive to investors.

On a trailing-12-month (TTM) basis ending in March 2024, S&P 500 (SNPINDEX: ^GSPC) companies completed $816.5 billion worth of buybacks, which is technically down from a TTM peak of $1.01 trillion for the period ended June 2022, based on data from S&P Global.

More importantly, 50.9% of the buybacks completed in the first quarter of 2024 were traced to the 20 largest companies by market cap in the S&P 500. Buybacks have been used to fuel earnings growth for America’s largest and most-influential businesses, but this isn’t guaranteed to continue if Harris wins in November and has the votes on Capitol Hill to increase the corporate tax rate by a third.

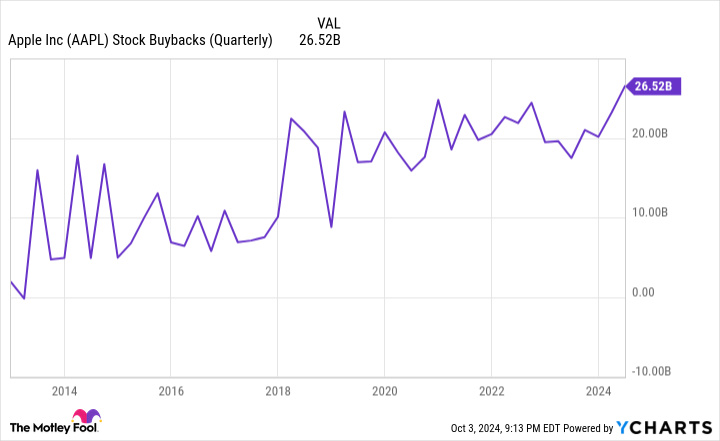

As an example, the world’s largest publicly traded company by market cap, Apple (NASDAQ: AAPL), has repurchased $700.6 billion worth of its common stock since the start of 2013 and reduced its outstanding share count by 42.2% in the process.

If Apple hadn’t bought back a single share over the last 11 years, its consensus EPS for fiscal 2024 (ended Sept. 30) would be less than $4 and not the current $6.68. Arguably no company’s bottom line has been fueled more in recent years by share repurchases than Wall Street’s largest public company.

If there’s a silver lining to this concern, it’s that a study from Fidelity found that the benchmark S&P 500 rose by an average of 13% following every corporate tax hike since 1950. While this doesn’t guarantee that stocks would rise if Harris increased the corporate tax rate from 21% to 28%, history strongly favors a continuation of the current bull market.

This might be even more worrisome than the prospect of reduced share buybacks

Although share repurchases have been artificially increasing EPS for Wall Street’s biggest companies for years, and a higher corporate tax rate could slow buyback activity, this might not be the most immediate concern for Wall Street. Rather, a historically pricey stock market could be the catalyst that tips equities into a correction or bear market, regardless of who’s elected president on Nov. 5.

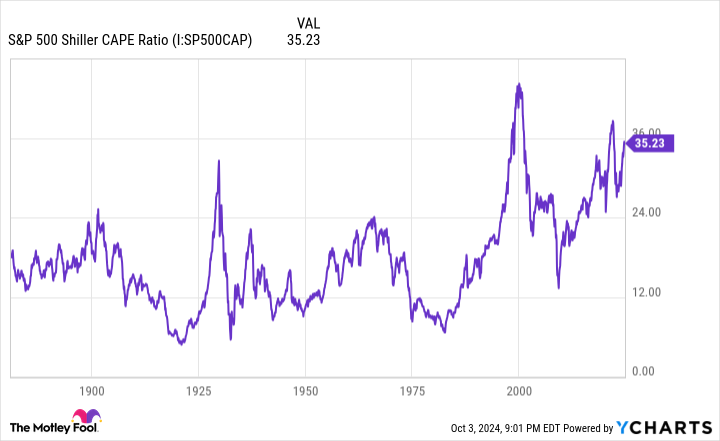

To be fair, there are a lot of ways for investors to measure value, and everyone has differing levels of risk tolerance. But based on readings from the S&P 500’s Shiller price-to-earnings ratio (P/E), we’ve witnessed only a handful of instances in more than 150 years where stocks have, collectively, been this pricey. The Shiller P/E ratio is also known as the cyclically adjusted price-to-earnings ratio, or CAPE ratio.

Most investors rely on the traditional P/E ratio as a quick and easy way to determine if a stock is relatively cheap or pricey when compared to its peers and its own history. However, the traditional P/E ratio only takes TTM earnings into account, which can be skewed or adversely affected by shock events, such as the temporary lockdowns that occurred during the pandemic.

The Shiller P/E ratio is based on average inflation-adjusted earnings from the previous 10 years. Encompassing a full decade of EPS history minimizes the impact of shock events, which leads to a more accurate measure of value.

When the closing bell tolled on Oct. 3, the S&P 500’s Shiller P/E stood at 36.6, which is more than double its average reading of 17.16, when back-tested to January 1871. Even though lower interest rates and the internet’s democratizing access to information have increased the willingness of everyday investors to take risks, a Shiller P/E of nearly 37 is an outsize reading.

Looking back to 1871, there have been only six total instances where the S&P 500’s Shiller P/E surpassed 30 during a bull market rally, including the present. Following the previous five occurrences, the S&P 500, Dow Jones Industrial Average (DJINDICES: ^DJI), and/or Nasdaq Composite (NASDAQINDEX: ^IXIC), shed between 20% and 89% of their value.

Though the Shiller P/E isn’t a timing tool — i.e., stocks can remain pricey for weeks, months, or in rarer cases multiple years — it does have a flawless track record of foreshadowing big declines in the S&P 500, Dow, and Nasdaq Composite.

While it’s possible Kamala Harris’ plan to raise the corporate tax rate by 33% would be bad news for Wall Street, the biggest enemy for investors right now is historically expensive stock valuations — and this is unlikely to change anytime soon.

Should you invest $1,000 in S&P 500 Index right now?

Before you buy stock in S&P 500 Index, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and S&P 500 Index wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $765,523!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of September 30, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple and S&P Global. The Motley Fool has a disclosure policy.

The Subtle Reason Stocks Can Plunge if Kamala Harris Raises the Corporate Tax Rate by 33% was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel