Semiconductor stocks have been in fine form on the stock market since the beginning of 2023, thanks to the terrific demand for chips used to power artificial intelligence (AI) servers, smartphones, and personal computers, among other things. The PHLX Semiconductor Sector index has shot up a terrific 115% since the beginning of last year, driven by the outstanding gains that the likes of Nvidia have clocked during this period.

More specifically, Nvidia stock has multiplied 8x since the start of 2023, and its market cap now stands at $3.0 trillion. However, the stunning rally in Nvidia stock has made it expensive with a price-to-earnings (P/E) ratio of 73, significantly more expensive than the Nasdaq 100‘s average P/E ratio of 32.

But Nvidia may be able to justify its valuation in the long run thanks to the huge opportunity in the AI chip market, where it is the dominant player. However, there is another semiconductor stock that is much cheaper and also enjoying healthy growth in this industry: Taiwan Semiconductor Manufacturing (NYSE: TSM). Popularly known as TSMC, the foundry giant could soon join Nvidia in the trillion-dollar market cap club.

Let’s look at the reasons why TSMC is on the path to becoming a trillion-dollar company.

The AI chip boom has given TSMC a big boost

TSMC released its second-quarter results on July 18. The foundry giant’s revenue increased 33% year over year to $20.8 billion, exceeding management’s guidance. It reported adjusted earnings of $1.48 per share for the quarter, up 30% year over year. It is worth noting that TSMC’s operating margin of 42.5% was also above the forecast range of 40% to 42%.

More importantly, TSMC’s outlook also exceeded expectations. The company is expecting third-quarter revenue to land between $22.4 billion and $23.2 billion. The midpoint of this range represents 45% year-over-year growth, a marked acceleration from last quarter. TSMC credits “strong smartphone and AI-related demand for our leading-edge process technologies” as the reason behind its bullish outlook.

A closer look at TSMC’s revenue breakdown indicates advanced chip nodes produced 67% of its wafer revenue, up from 53% in the same quarter last year. Advanced chip nodes are defined as process technologies that are 7 nanometers or lower in size. TSMC currently has three such advanced chip nodes in the form of 7nm, 5nm, and 3nm processes.

The 5nm node was the biggest seller last quarter with its revenue share climbing five percentage points to 35%. It is worth noting that the smaller the process node, the more powerful the chip. TSMC introduced a 3nm node in the past year, and it already accounted for 15% of second-quarter revenue, further illustrating how the demand for TSMC’s advanced chip technologies is increasing.

Moreover, chipmakers are using advanced process nodes to design AI chips. Nvidia’s popular H100, for instance, is based on a 5nm process node. Even Intel and AMD are deploying 5nm chips to manufacture their AI accelerators, while these chipmakers are also looking to move to the more advanced 3nm process node in the near future.

The market for AI chips is forecast to expand at a compound annual growth rate of 26% over the next decade, generating $287 billion in revenue at the end of the forecast period, according to a report from Future Market Insights. As the leading foundry services provider in the world with a market share of 62% in Q1, TSMC seems to have a bright future ahead of it.

TSMC’s valuation and growth hint at a trillion-dollar market cap

TSMC has a market cap of $885 billion as of this writing, which means it needs just 13% share price growth to hit the $1 trillion milestone. The stock has a 12-month median price target of $200 per the 41 analysts covering the stock, implying an 18% jump from current levels. Following its latest quarterly report, TSMC could reach $1 trillion sooner rather than later.

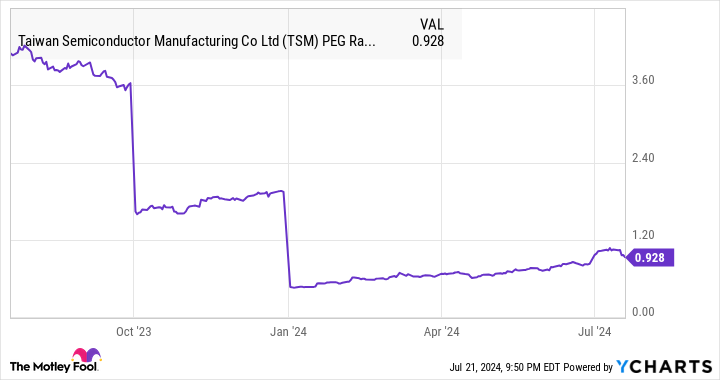

What’s more, TSMC’s earnings are expected to grow at an annual rate of 21% for the next five years, but it trades at just 30 times trailing earnings, a discount to Nasdaq 100 index. Its price/earnings-to-growth ratio (PEG ratio), which factors in a company’s growth prospects, is less than 1, a common indicator of an undervalued stock.

In TSMC, investors get a rare combination of value and growth, and they should take a closer look at this top AI stock before it adds to the 65% gain it has already clocked in 2024.

Should you invest $1,000 in Taiwan Semiconductor Manufacturing right now?

Before you buy stock in Taiwan Semiconductor Manufacturing, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Taiwan Semiconductor Manufacturing wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $700,076!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Intel and recommends the following options: long January 2025 $45 calls on Intel and short August 2024 $35 calls on Intel. The Motley Fool has a disclosure policy.

This Undervalued Stock Could Join Nvidia in the Trillion-Dollar Club was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel