As you may have noticed, the bulls are in firm control on Wall Street. The ageless Dow Jones Industrial Average (DJINDICES: ^DJI), benchmark S&P 500 (SNPINDEX: ^GSPC), and innovation-fueled Nasdaq Composite (NASDAQINDEX: ^IXIC) all recently notched fresh record-closing highs.

But it hasn’t always been this way. In each of the first four years of this decade, the Dow Jones, S&P 500, and Nasdaq Composite traded off bear and bull markets in successive years.

Though all three indexes have risen over long periods, forecasting short-term directional moves is something that investors can’t do with any guaranteed accuracy. Nevertheless, it doesn’t stop investors from trying to guess what the immediate future holds for stocks.

Even though the short term offers no certainties, there are a select number of predictive tools and forecasting metrics that have strongly correlated with moves higher or lower in the stock market throughout history. One such measure, which appears to portend a bumpy ride to come for the U.S. economy and Wall Street, is U.S. money supply.

U.S. money supply hasn’t done this since 1933

While there are a handful of U.S. money supply measures, the two most closely watched are M1 and M2.

M1 money supply takes into account all cash and coins in circulation, as well as demand deposits in a checking account. The best way to think of M1 is as money that can be accessed and spent at a moment’s notice.

Comparatively, M2 money supply factors in everything found in M1 and adds in savings accounts, money market accounts, and certificates of deposit (CDs) below $100,000. It’s still money you can spend with relative ease, but the capital in M2 requires a little more work to get in your hands. It’s this figure that’s the source of concern.

M2 has been rising with virtually no interruption for the better part of nine decades. This is what we’d expect to see from a growing economy that relies on more capital in circulation to facilitate transactions. But in those very rare instances throughout history where M2 money supply has notably declined, trouble has followed for the U.S. economy and stocks.

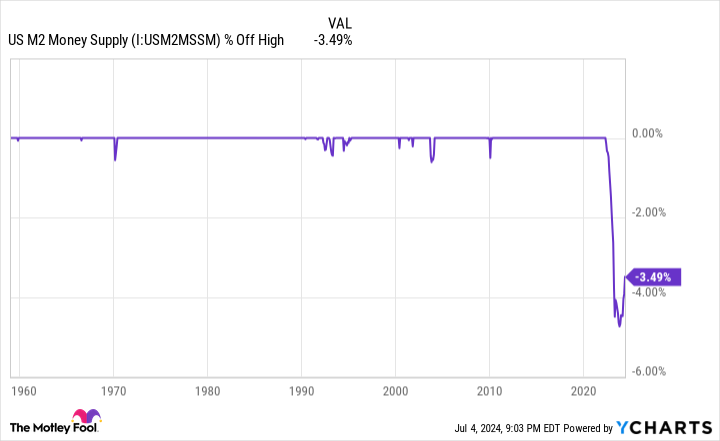

According to monthly reported data from the Board of Governors of the Federal Reserve, M2 money supply peaked in April 2022 at $21.722 trillion. As of May 2024, M2 totaled $20.963 trillion. This $759 billion decline in a little over two years represents a 3.49% aggregate drop. It’s the first time a greater than 2% cumulative decline in M2 money supply has occurred since the Great Depression.

While I’ll touch on the historical significance of this drop in a moment, there are some asterisks that can, and should, be addressed.

For starters, this 3.49% drop comes after U.S. M2 money supply expanded by more than 26% on a year-over-year basis during the height of the COVID-19 pandemic. Money absolutely poured into the U.S. economy from the federal government via stimulus checks, and the Fed was extremely accommodative with historically low interest rates. The cumulative decline in M2 following a record surge might represent nothing more than a return to the norm.

Additionally, M2 money supply is now rising on a year-over-year basis. As of the May 2024 reading, M2 has increased by 0.82% from the prior-year period. This has reduced the aggregate drop from a peak decline of 4.74% in October 2023 to the noted 3.49%.

Despite these asterisks, history portends trouble for the U.S. economy and Wall Street when M2 declines by at least 2% on a year-over-year and cumulative basis.

WARNING: the Money Supply is officially contracting. 📉

This has only happened 4 previous times in last 150 years.

Each time a Depression with double-digit unemployment rates followed. 😬 pic.twitter.com/j3FE532oac

— Nick Gerli (@nickgerli1) March 8, 2023

The post you see above on social media platform X comes courtesy of Reventure Consulting CEO Nick Gerli. Although this post is more than a year old, it serves a valuable purpose in laying out the correlation between declines in M2 money supply and the poor performance of the U.S. economy.

When back-tested to 1870, there have only been five instances when year-over-year M2 money supply has declined by at least 2%: 1878, 1893, 1921, 1931-1933, and 2023. The first four instances match up with periods of depression and double-digit unemployment rates for the U.S. economy.

To be fair, things were a lot different in the late 19th and early 20th centuries than they are today. The first two depressions occurred before there was a Federal Reserve, and the latter two arrived not long after its creation. In the nine decades since the Great Depression took shape, the U.S.’s central bank and federal government have effectively learned how to combat economic downturns and/or high periods of unemployment. While the chance of a depression in the modern era isn’t zero, a sustained steep downturn is highly unlikely.

Nonetheless, meaningful declines in M2 money supply have historically signaled that consumers and businesses will need to pare back their spending. In short, it tends to be a key ingredient of an economic downturn or full-blown recession.

Based on historical data, approximately two-thirds of the S&P 500’s peak-to-trough downturns occur during, not prior to, a U.S. recession being declared by the National Bureau of Economic Research.

History is a two-sided coin that isn’t linear and strongly favors the patient

Make no mistake about it, M2 isn’t the only concerning metric right now for the U.S. economy or Wall Street. As I recently pointed out, the longest yield-curve inversion of the modern era, along with one of the priciest valuation readings in the history of the S&P 500, would appear to bode poorly for investors.

Thankfully, the most important thing for investors to remember is that history is a pendulum that swings in both directions and isn’t linear.

As an example, slowdowns and recessions are a normal and inevitable aspect of the economic cycle. No matter how much we dislike and/or wish away the rise in unemployment and lack of wage growth that accompanies recessions, they’re going to occur from time to time.

On the other hand, recessions are decisively short-lived. Since World War II ended in September 1945, the U.S. economy has worked its way through a dozen recessions. Nine of these economic downturns were resolved in less than a year, with the remaining three failing to surpass 18 months in length. Meanwhile, most periods of economic expansion have endured multiple years, with two reaching the 10-year mark since September 1945.

The economic cycle isn’t linear, and neither are bear and bull markets on Wall Street.

A little more than a year ago, the researchers at Bespoke Investment Group published the data set you see above on X that details every bear and bull market in the broad-based S&P 500 dating back to the start of the Great Depression in September 1929. All told, Bespoke calculated the calendar-day length of 27 separate bear and bull markets.

While the average S&P 500 bear market lasted about 9.5 months (286 calendar days), the typical bull market over the prior 94 years stuck around for roughly two years and nine months (1,011 calendar days). It’s also worth noting that nearly half (13 of 27) of the S&P 500 bull markets since September 1929 lasted longer than the lengthiest bear market, which stuck around for 630 calendar days (Jan. 11, 1973-Oct. 3, 1974).

Even though we’re never going to know ahead of time when potentially mammoth moves lower in the stock market will begin or how long they’ll last, history couldn’t be clearer that patience and perspective are a winning combination on Wall Street. If you’re a long-term-minded investor and lean on time as an ally, an aggregate decline of 3.49% in M2 money supply is nothing to be overly concerned about.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

-

Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $22,525!*

-

Apple: if you invested $1,000 when we doubled down in 2008, you’d have $42,768!*

-

Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $372,462!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of July 2, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

U.S. Money Supply Has Done Something So Rare That It Hasn’t Occurred Since the Great Depression — and a Mammoth Move in Stocks May Follow was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel