Share prices of Dell Technologies (NYSE: DELL) have shot up an impressive 190% in the past year, but its red-hot rally hit an iceberg on May 30 following the release of the company’s fiscal 2025 first-quarter results (for the three months ended May 3).

Dell’s stock price plunged 18% in a single session following the earnings report release. Dell reached its latest 52-week high on May 29, and it has lost nearly 24% of its value since then.

Let’s see why investors pressed the panic button following Dell’s latest report, and check if it could be a buying opportunity for investors.

Dell’s AI investments are hurting its bottom line

Dell reported fiscal Q1 revenue of $22.2 billion, an increase of 6% over the prior-year period. The company’s top line exceeded the higher end of its guidance range of $21 billion to $22 billion, and it was also better than the $21.6 billion consensus estimate. However, Dell’s non-GAAP earnings in Q1 fell 3% year over year to $1.27 per share, though they were better than the $1.23 per share Street estimate.

Dell’s gross margin fell 250 basis points last quarter thanks to “a more competitive pricing environment and a higher AI optimized server mix.” What this indicates is that Dell is pricing its personal computers (PCs) more competitively to capitalize on the turnaround in this market. At the same time, Dell’s focus on ramping up the production of AI-optimized servers is hurting its margins as well.

So even though Dell’s quarterly revenue increased for the first time since 2022, its earnings went in the other direction. Dell now expects its full-year revenue to increase by 8% to $95.5 billion, compared to the earlier expectation of $93 billion. Analysts were expecting Dell to finish the year with a 7% increase in revenue.

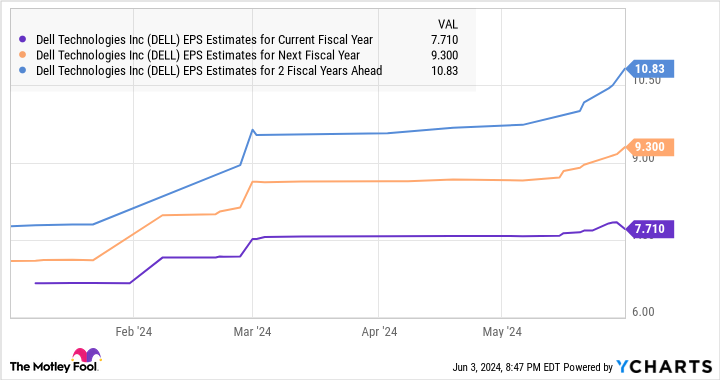

However, Dell’s forecast of a 7% increase in adjusted earnings to $7.65 per share missed the $7.70 per share consensus estimate. CFO Yvonne McGill explained why that’s going to be the case on the latest earnings conference call:

Given inflationary input costs, the competitive environment and higher mix of AI optimized servers, we do expect our gross margin rate to decline roughly 150 basis points though we expect both ISG and CSG operating margin rates to be within our long-term financial framework for the full year.

So Dell’s margins are set to shrink in the near term. However, a closer look at the company’s artificial intelligence (AI)-fueled growth and opportunities indicates that the pain should be temporary.

The AI revenue pipeline points toward better times

Dell’s revenue was down 14% in fiscal 2024 (which ended on Feb. 2, 2024). Additionally, its earnings fell 6%. So the company’s fiscal 2025 forecast makes it clear that it is set to return to growth this year, and AI is playing a central role in that turnaround.

For instance, Dell’s revenue from the infrastructure solutions group (ISG), which includes sales of server and storage solutions, shot up an impressive 22% year over year in the previous quarter to $9.2 billion. The company sold $1.7 billion worth of AI servers last quarter, a sequential increase of over 100%. Dell management points out that it has sold more than $3 billion worth of AI servers in the past three quarters.

More importantly, customers continue to place more orders for Dell’s AI servers. This is evident from the company’s AI server backlog of $3.8 billion at the end of the previous quarter, up by $900 million on a sequential basis. Even better, Dell management claims that its “AI optimized server pipeline grew quarter over quarter again and remains a multiple of our backlog.”

The company has seen a jump in the number of enterprise customers that are buying AI servers and expects this trend to drive growth in the long run considering that AI adoption is currently in its early phases. Global Market Insights forecasts an 18% annual increase in the AI server market’s revenue through 2032, when it is expected to generate annual revenue of $177 billion, compared to $38 billion in 2023.

As such, there is a good chance that Dell’s ISG business will be able to sustain its impressive growth over the long run and boost its top and bottom lines. This probably explains why analysts forecast a nice bump in the company’s earnings growth over the next couple of fiscal years following fiscal 2025’s single-digit jump.

Shares of Dell trade at 28 times trailing earnings and 18 times forward earnings, which represents a discount to the U.S. technology sector’s price-to-earnings ratio of 43. So investors are getting a steal of a deal on this AI stock that could deliver solid returns in the long run on the back of a potential acceleration in its earnings growth.

Should you invest $1,000 in Dell Technologies right now?

Before you buy stock in Dell Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dell Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $741,362!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of June 3, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

1 No-Brainer Artificial Intelligence (AI) Stock Down 26% to Buy Hand Over Fist Right Now was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel