The last 15 months have been a fantastic time to own stocks. The last 15 years, if we’re really being honest. In this most recent run, an artificial intelligence (AI) boom and soaring profits for technology companies have helped the stock market indexes break through to new highs multiple times in 2024.

Investors also appear excited to once again place bets on money-losing start-ups. In that way, the market feels eerily similar to 2021. While stocks might be soaring today, this is a dangerous time to buy growth stocks. Countless examples of so-called “hot” stocks back in 2020 and 2021 are down 90% (or worse) today from their all-time highs. It is imperative as an individual investor that you learn from recent history and stay rational with your personal investment portfolio.

Here are two consumer stocks that I wouldn’t touch with a 10-foot pole. Each has a large potential downside over the next few years.

1. Opendoor: Flawed from the start

The first stock on my list is Opendoor Technologies (NASDAQ: OPEN). The start-up aims to use an online platform to buy and sell residential real estate. It went public back in 2020. Today, shares are off 93% from all-time highs. However, I think there is likely more pain ahead for Opendoor shareholders.

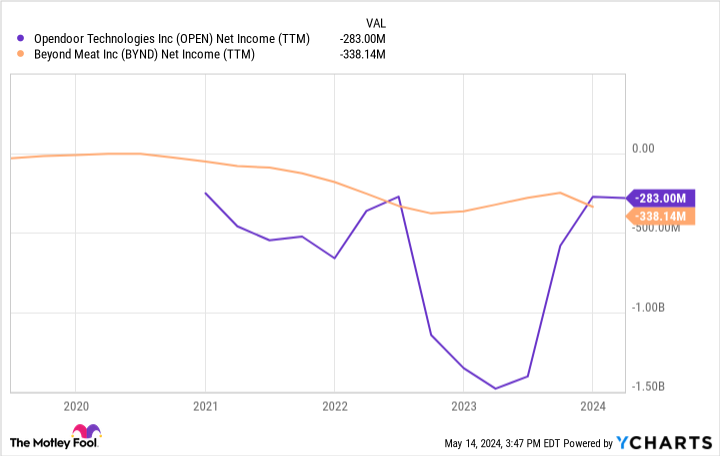

Why? First, Opendoor has never been profitable. Over the last 12 months, it posted negative $283 million in net income on $431 million in gross profit. Revenue declined 62% year over year in the first quarter of 2024 as management shrank operations to stay in business. The financials are ugly, and with revenue moving in the wrong direction, it is hard to see how Opendoor will turn a profit anytime soon.

Buying and selling real estate through an online portal was a flawed business model from the start. The jump in interest rates in 2022 made that even more apparent. While friction in homebuying was reduced by the likes of Zillow, Opendoor is not solving any issues for consumers. It is also a capital-intensive business that needs to be financed by debt. As Opendoor grows, it has to add more real estate inventory to its balance sheet, which eats up a lot of its cash and makes the business difficult to run.

It is no surprise then to see Opendoor’s book value per share off 68% from all-time highs to $1.30. Book value per share tells investors the net worth of Opendoor’s balance sheet and is important for an asset-heavy business. What should spook investors is that Opendoor trades at a stock price of $2.50, which is close to twice its book value per share. A book value that continues to decline quarter after quarter.

There are no redeeming qualities to Opendoor’s business model, even if interest rates begin to come down again. Don’t take a flyer on this stock, even though it has a low share price. There could be much more downside ahead.

2. Beyond Meat: Where is the growth?

The only company with a more troubled business than Opendoor may be Beyond Meat (NASDAQ: BYND). The plant-based meat start-up went public back in 2019 during the craze over plant-based meat substitute companies. Investors were excited about these new technologies and what it could mean if these new foods could disrupt the traditional meat sector.

Turns out that these dreams never really materialized. Beyond Meat’s revenue has been falling for multiple years now, with terrible margins to boot. Last quarter, revenue declined 18% year over year while gross margins fell to a measly 4.9%. This means the company has to heavily discount its products and is barely selling them above cost.

Unsurprisingly, this has led to some bad profit figures. Net income has been negative since 2020, and the stock is now down 96% from all-time highs. But it doesn’t look like there is any relief on the horizon. Surveys indicate that the popularity of fake meat products is declining among consumers, which could mean even more pain for Beyond Meat in the years ahead.

No growth, terrible margins, and a bleak industry outlook. Beyond Meat is in a dire situation. Stay far away from this stock.

Should you invest $1,000 in Beyond Meat right now?

Before you buy stock in Beyond Meat, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Beyond Meat wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Beyond Meat, Opendoor Technologies, and Zillow Group. The Motley Fool has a disclosure policy.

2 Consumer Stocks I Wouldn’t Touch With a 10-Foot Pole was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel