You already know the basics of building wealth in a 401(k) account, right? These game-changing tactics have been shared a million times, because they are undeniably powerful and always a good idea:

-

Max out your 401(k) contributions every month.

-

Contribute enough to receive the full employer match, too.

-

Get started as early as possible and leave your money untouched for as long as you can.

I mean, yeah. Sticking to these principles forever will almost certainly make you a millionaire someday. The strategy is both tried and true. The details will vary with your annual salary, the cost of living in your area, the percentage your employer will add to your 401(k)-bound paycheck deductions, boom and bust cycles in the future economy, and more.

In most cases, staying true to these three golden rules for at least three decades will probably get you a card to the millionaire club in the end.

But did you know that you can reach that million-dollar goal without pushing the pedal all the way to the metal?

It’s true. You can make a million in your 401(k) retirement savings account without maxing out the key principles above. The overarching secret to the millionaire-making retirement strategy is that it’s easier than you think.

On that note, let me show you three simple ways you can get away with lowering your effort and still retire as a millionaire.

Reasonable assumptions

Every situation is unique, so I can’t review every possible complication here. I can set up some reasonable assumptions based on national averages, though. As you’ll soon find out, there’s wiggle room with every metric and you should spend some time with a handy 401(k) calculator, like this CalcXML tool:

*Calculator is for estimation purposes only, and is not financial planning or advice. As with any tool, it is only as accurate as the assumptions it makes and the data it has, and should not be relied on as a substitute for a financial advisor or a tax professional.

To use this calculator, you’ll need to input some key information, including:

-

The number of years you have until retirement

-

Your current 401(k) balance

-

Your current 401(k) contribution, as a percentage of your salary

-

Your employer’s 401(k) match

-

Your anticipated returns on your 401(k) investments prior to and during retirement

-

The length of time you expect to need money in retirement

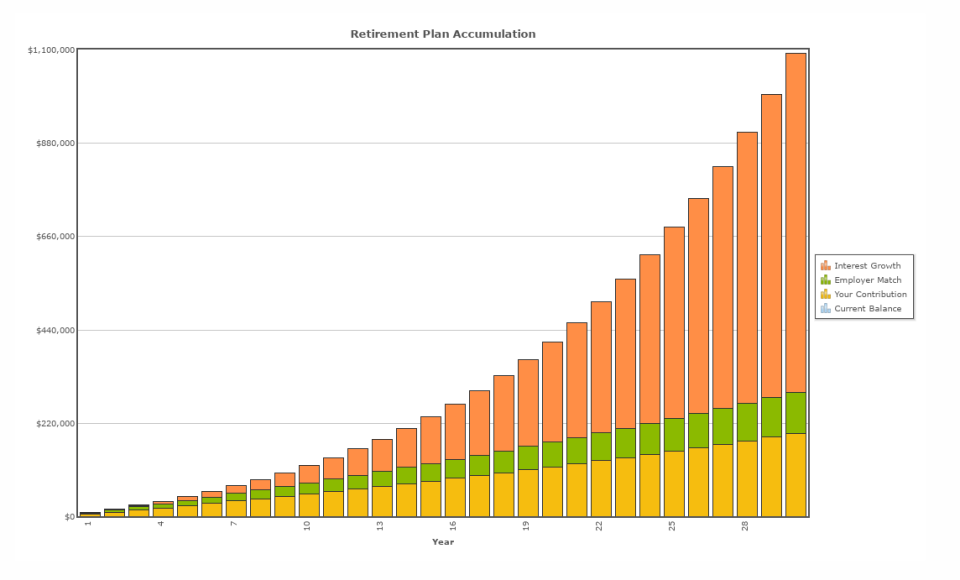

For the discussion below, I’m working with a base case of 30 years until retirement (from age 35 to 65, for example), current annual income of $60,000, annual salary increases of 2%, no starting funds in the 401(k) account, and contributing 8% of your annual pay to the 401(k) plan with a 50% employer match (which works out to 4% of your annual pay).

These numbers are close to national averages, erring on the conservative side. Unless otherwise noted, I left the remaining default figures untouched. The “moderate” case with annual investment returns of 8% lands at a total value of $1.1 million in 30 years — just a hair above the million-dollar target balance.

1. Time in the market beats everything else

In my example, you’ll contribute $4,800 in the first year — let’s call it 2024 — and $6,470 in 2054. Matching contributions from your employer will start at $2,400 and reach $3,235 in the last year. Your cumulative money contributions add up to nearly $300,000.

In other words, more than two-thirds of your nest egg will be the result of investment returns.

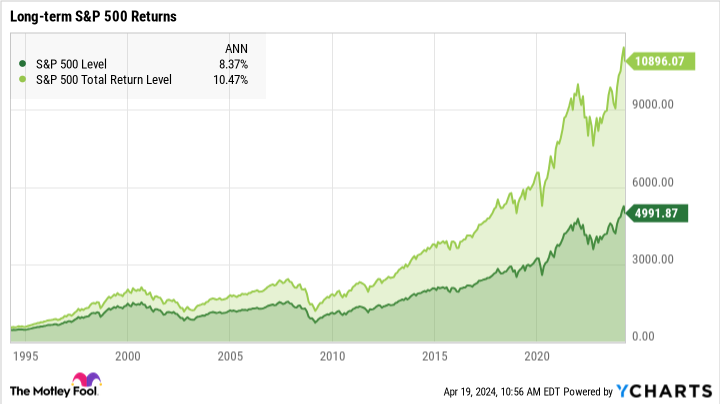

And that’s just the “moderate” scenario with a compound annual growth rate of 8%. In reality, the S&P 500 (SNPINDEX: ^GSPC) market index has delivered an 8.4% CAGR over the last 30 years, a period including some of the worst market dips in history. And if you had the foresight to reinvest dividends along the way, you’d have an annual return of 10.5%:

The dividend-boosted long-term average is close to the “aggressive” returns in the example above. That’s worth nearly $2 million after 30 years. So even the modest investment rates I’m looking at should easily beat the million-dollar goal in three decades.

2. You don’t always need “market-beating returns” or exceptional investment ideas

Yes, your wealth can grow faster if your particular 401(k) plan lets you select individual stocks, and you happen to find some big winners. Maybe you work for Apple (NASDAQ: AAPL) or Microsoft (NASDAQ: MSFT), who offer robust 401(k) options with market-trouncing stock returns in the long run. Extra money is always better, of course. But you can still be a 30-year millionaire without winning the stock-picking lottery.

3. ETFs can make it simple to match long-term market returns

All you need is a simple exchange-traded fund (ETF) tracking a solid market index with low annual fees.

The Vanguard S&P 500 ETF (NYSEMKT: VOO) springs to mind, offering a near-perfect match to the leading market index’s returns with microscopic management fees and a super-simple dividend reinvestment function.

It’s also pretty safe to track American blue-chip stocks with Dow Jones Industrial Average ETF Trust (NYSEMKT: DIA). More ambitious investors could opt for the Invesco QQQ Trust (NASDAQ: QQQ), which follows the NASDAQ Composite Index — a more volatile option that tends to outperform the S&P 500 when the time period is measured in decades.

Like the Vanguard S&P 500 ETF, these exchange-traded funds match the returns of solid market indices with low annual fees. Feel free to mix and match them, too. There are no wrong answers as long as you’re sticking with robust, low-fee performers.

And as the tool above shows, that’s all you need in the long run. Your future millionaire self will thank you for starting your 401(k) contributions today.

The $22,924 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

View the “Social Security secrets”

Anders Bylund has positions in Vanguard S&P 500 ETF. The Motley Fool has positions in and recommends Apple, Microsoft, and Vanguard S&P 500 ETF. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

3 Secrets of 401(k) Millionaires was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email [email protected] Follow our WhatsApp verified Channel