E-commerce and cloud giant Amazon (NASDAQ:AMZN) is poised for the next decade of growth after delivering a return of around 1,000% over the last decade. Thanks to its recent earnings beat, the stock price recently hit a new all-time high. Despite these gains, Amazon’s reaccelerated AWS growth, bolstered by AI, strong retail momentum, and margin and cash-flow expansion from optimization initiatives, make me bullish on the stock. Thus, I’ll buy the stock at current levels.

Amazon Posts Yet Another Quarterly Beat Driven by AWS

On April 30, Amazon reported impressive Q1 results for the fifth consecutive quarter, driven by upbeat performance across all segments, including cloud, advertising, and e-commerce. Adjusted earnings of $0.98 per share handily beat analysts’ estimates of $0.84 per share. Also, earnings more than trebled (+216%) year-over-year compared to earnings of $0.31 per share in the prior-year period.

Further, net sales soared 13% year-over-year to $143.3 billion, and sales for Amazon’s cloud business segment, Amazon Web Services (AWS), grew 17% year-over-year to $25 billion, beating expectations. Segment growth was aided by renewed demand and investments in generative AI, which boosted AWS’s performance, alongside a near cessation of the cost optimizations that customers had resorted to last year.

Particularly noteworthy is that AWS’s operating income jumped 84.3% year-over-year to $9.4 billion. Further, there was a significant operating margin expansion in the segment from 24% in the prior-year quarter to 37.6% currently.

Region-wise, North America sales grew 12% year-over-year, with International segment revenue growth at 11% (in constant currency). Moreover, operating income for all the company’s segments combined jumped by 219% year-over-year to $15.3 billion.

Based on its robust Q1 performance, Amazon provided an optimistic Q2 outlook, above expectations. Q2 net sales are projected to grow between 7-11% to be in the range of $144-149 billion. Notably, operating income guidance of $10-14 billion ($12 billion at the midpoint) is also much higher compared to the $7.7 billion generated in the first quarter of 2023.

AWS Sees Record Growth and Margins in Q1 Due to AI Impact

AWS, Amazon’s cloud business, has long been the market leader and the profit engine for the company for years. However, after years of impressive growth, the segment saw a slowdown, with growth decelerating to 13% in 2023 compared to 29% in 2022 and 37% in 2021.

That downtrend is now history. In Q1, AWS’s sales grew 17%, helping AWS reach the much-anticipated $100 billion run rate milestone in revenues. Additionally, operating income for the segment saw a remarkable growth of 84%.

Artificial intelligence (AI) is the catalyst behind this stupendous growth witnessed at AWS during the quarter. As a matter of fact, the tech titans of the world like Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOGL) (NASDAQ:GOOG) have been investing heavily in AI technology.

For instance, Microsoft’s Azure has gained market share in the cloud space, now holding a 25% share versus 19% in 2021. The addition of AI tools has been a contributing factor toward Azure’s rapid growth over the years. Like its peers, Amazon is making meaningful investments in AI and developing its own large language models as well as investing billions in AI products like Anthropic (which competes with OpenAI’s ChatGPT).

Amazon’s investments in AI are now reaping benefits and showing up in the financial figures. The company stated that the majority of its FY2024 CapEx (capital expenditures) will be toward bolstering AWS infrastructure and AI efforts. As the cloud leader, AWS can significantly monetize the growing demand for AI with its wide variety of cloud offerings.

It’s not just the margin expansion that impressed investors in Q1. It was a huge jump in cash flows despite substantial capital investments in AI and cloud infrastructure. This reassured investors that Amazon’s fundamentals remain intact. Q1 free cash flows grew to $50.1 billion (Q4: $36.8 billion) compared to cash outflows of $3.3 billion a year ago. Margin expansion, coupled with robust free cash flows, implies strong returns for investors in the years to come.

Earlier this week, there was news that AWS is looking to invest billions in Italy to strengthen its cloud infrastructure and data center operations in the country. Similarly, AWS will invest billions in Spain (€15.7 billion) and Germany (€7.8 billion) with the aim of expanding its cloud business across European countries.

Amazon has been undertaking key initiatives to streamline the company’s operations as well as bring down costs. These steps include transforming the U.S. fulfillment model from a nationwide one to a regional one and synchronizing inventory with the regional consumers, among others.

On a separate note, Amazon recently announced the departure of its AWS head, Adam Selipsky. He will be replaced by Matt Garman, an AWS veteran, to become the CEO of AWS. This leadership change may further enhance Amazon’s AI growth initiatives.

Amazon’s Valuation Isn’t Expensive

As Amazon houses multiple businesses under its radar, I believe the EV/EBITDA ratio is the best metric to evaluate the stock’s valuation. Being an industry leader, the company has historically traded at high multiples. At present, however, Amazon stock is trading at around 14.3x EV/EBITDA (on a forward basis) compared to its own five-year historical average of 20.6x. This implies a huge 31% discount.

For the sake of comparison, let’s also look at its P/S ratio. Amazon is trading at a price-to-sales (P/S) ratio of 3.0x. In contrast, cloud computing and tech giant Microsoft trades at a P/S of 13.1x, while social networking company Meta Platforms (NASDAQ:META) trades at a P/S of 7.7x.

Therefore, I believe the stock is trading at an attractive valuation and presents a great buying opportunity, given the strong growth potential across various business verticals.

Is Amazon Stock a Buy, According to Analysts?

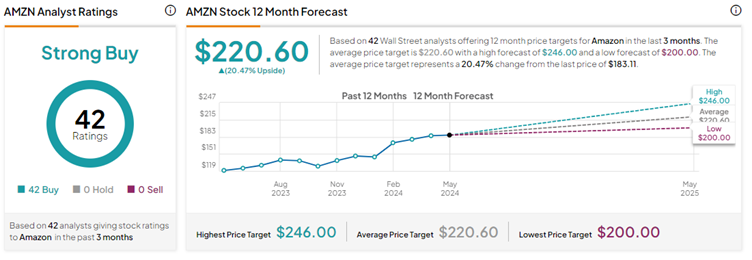

Wall Street analysts continue to be bullish on Amazon stock, with a majority of them raising their price targets after the impressive earnings beat. Overall, the stock commands a Strong Buy consensus rating based on 42 unanimous Buys. Amazon stock’s average price target of $220.60 implies 20.5% upside potential from current levels.

Conclusion: Consider AMZN Stock for Its Long-Term Growth

Amazon may have been a little late to the AI growth story, but it’s important to remember that AWS remains the leader in cloud infrastructure. Its substantial investments and recent leadership changes should yield significant benefits. The foundation has been laid, and I believe there’s no turning back for Amazon.

With multiple growth drivers, including AWS’s growth trajectory fueled by generative AI initiatives, a well-diversified business portfolio, strong retail performance, and impressive margin and cash-flow expansion, Amazon appears well-positioned for its next phase of growth. Therefore, I am confident in buying the stock at its current levels.

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel