While artificial intelligence (AI) is attracting investors’ attention, there’s another massive trend they should be aware of: cybersecurity. Bad actors have never had more tools, and the amount of digital information that can be accessed is also growing. This isn’t a trend that’s going away, either; companies must ensure they have top-notch security or risk being the target of a cyberattack, which can cost millions and destroy confidence in a company.

As a result of this new reality, the cybersecurity industry is seeing a massive boom. But with so many cybersecurity companies available to choose from, it’s easy to get lost. One company is my clear choice, and it has the potential to become a much larger force in this industry.

CrowdStrike has become a top pick in the cybersecurity space

CrowdStrike (NASDAQ: CRWD) is my top pick in the cybersecurity space for many reasons. First, it’s a lightweight cloud-native program. This means it can be easily deployed to all endpoints in a business network quickly and doesn’t take much bandwidth. Additionally, CrowdStrike has integrated AI into its product lineup since its launch.

Unlike some companies that use AI as a buzzword, CrowdStrike’s platform is built on it. Its primary product in the Falcon platform is endpoint protection. This protects network access points like laptops or cellphones from outside threats, and CrowdStrike utilizes AI to analyze activity to understand if it’s normal or a threat. It can terminate access to a company’s server without human intervention if it detects a threat.

It also has its Charlotte AI, a generative AI product. This allows users to automate workflows, accelerate investigation time, and reduce the amount of skill required to become a cybersecurity expert. Based on a customer survey, Charlotte helps save around two hours per day through increased efficiency.

CrowdStrike has a massive product line that has slowly grown over the past few years. Instead of having to piece together cybersecurity solutions from various vendors, CrowdStrike is working toward becoming a one-stop shop for all cybersecurity needs. With products in endpoint protection, cloud security, identity protection, threat intel, and more, CrowdStrike covers many areas.

This strategy has worked for CrowdStrike, as 64% of customers utilize at least five modules, and 27% utilize at least seven. This shows plenty of room for product expansion among its client base, so upselling existing customers and signing new ones gives CrowdStrike two growth avenues.

CrowdStrike’s stock has gotten expensive

Speaking of growth, CrowdStrike has been delivering excellent growth for some time. In the fourth quarter of fiscal-year 2024 (ending Jan. 31), its annual recurring revenue (ARR) rose 34% year over year to $3.44 billion. Looking forward to FY 2025, CrowdStrike expects revenue growth of 30% to nearly $4 billion. Despite CrowdStrike getting larger, its growth is hardly slowing down, which is a testament to the demand in the cybersecurity industry and CrowdStrike’s prowess. Wall Street analysts even believe it can grow revenue at a 27% pace in FY 2026 to over $5 billion.

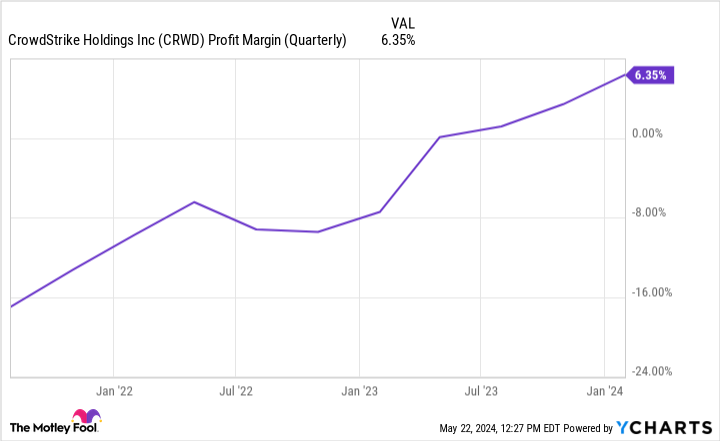

CrowdStrike is also becoming increasingly profitable each quarter.

So you’ve got a company that is an industry leader in a rapidly expanding field and has excellent financials. It seems like a no-brainer buy, right?

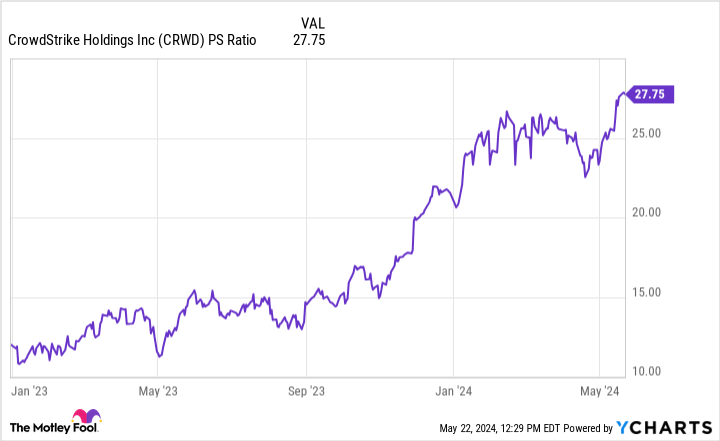

Investors must also consider the price tag of the stock. It’s no secret that CrowdStrike is an excellent company, and its stock is priced accordingly.

A price of 28 times sales is very expensive, which is the primary drawback of CrowdStrike’s stock. I’m using the price-to-sales (P/S) ratio because CrowdStrike hasn’t reached maximum profitability yet. To translate into the more familiar price-to-earnings (P/E) ratio, I’ll give CrowdStrike an artificial 30% profit margin — a great goal for software companies like CrowdStrike.

With that profit margin, CrowdStrike would have a P/E of 93 at today’s prices. If you utilize analysts’ FY 2026 revenue projection of $5.03 billion, CrowdStrike would trade at 56 times earnings.

That’s too expensive for many investors’ taste, and I wouldn’t blame them for not buying at today’s prices. However, I’d keep CrowdStrike on your radar, as it’s too good of a company to forget about if the stock price drops to more reasonable levels.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for two decades, Motley Fool Stock Advisor, has more than tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now… and CrowdStrike made the list — but there are 9 other stocks you may be overlooking.

*Stock Advisor returns as of May 13, 2024

Keithen Drury has positions in CrowdStrike. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool has a disclosure policy.

Here’s My Top Cybersecurity Stock (and It’s Not Even Close) was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel