The Nasdaq Composite (NASDAQINDEX: ^IXIC) entered a new bull market in December 2022, roughly 17 months ago, and it has since advanced 68%. But history says more gains lie in store for the technology-heavy index. The Nasdaq returned an average of 215% during bull markets since 1990, and it achieved those gains over an average of 40 months.

In other words, if the current bull market aligns precisely with the historical average, the index will advance another 147% during the next two years. To be fair, that implies a somewhat unrealistic return of 57% annually. But patient investors still have reason to believe the Nasdaq is headed higher.

The index increased at 16.1% annually over the last decade, crushing the S&P 500‘s annual return of 12.9%, and similar results are possible in the coming years. To capitalize on that upward momentum, investors should consider buying small positions in Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL) and CrowdStrike (NASDAQ: CRWD). Here’s why.

1. Alphabet

Alphabet has two important growth engines: digital advertising and cloud computing. Its Google subsidiary is the largest ad tech company in the world due to its ability to engage consumers and collect data. Specifically, with six products that reach 2 billion monthly users — think Google Search, Chrome, and YouTube — the company can efficiently capture data that helps advertisers build more successful campaigns.

Likewise, Google Cloud Platform (GCP) is the third-largest provider of cloud infrastructure and platform services. While the company trails Amazon Web Services and Microsoft Azure by a wide margin, it gained a percentage point of market share over the past year and that trend could persist as businesses invest in artificial intelligence (AI). Admittedly, Microsoft has so far outmaneuvered its peers where generative AI is concerned, but Google is a long-standing leader in AI research and its technological prowess should not be underestimated.

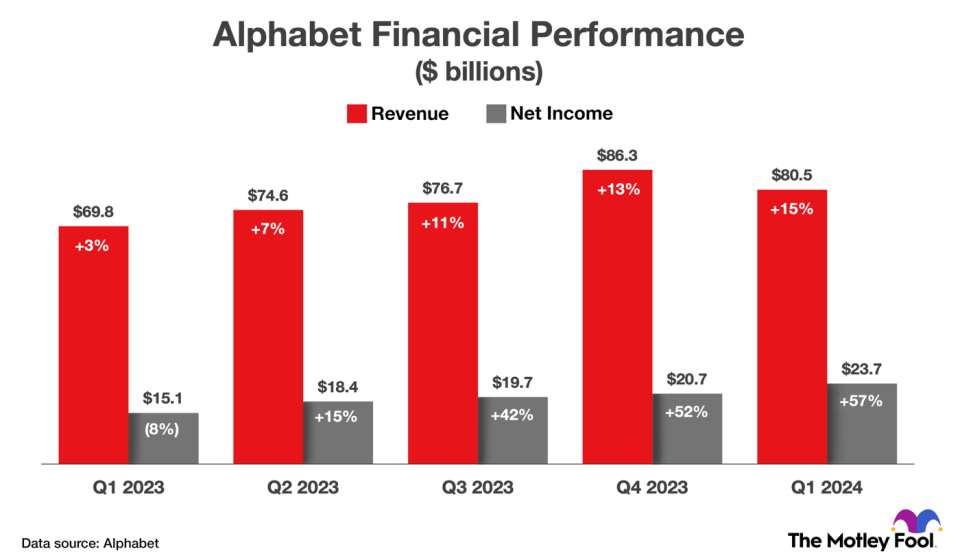

In the first quarter, Alphabet reported its fourth consecutive acceleration in top- and bottom-line growth, as shown in the chart below. Revenue increased 15% to $80.5 billion due to especially strong growth in Google Cloud, the segment comprising cloud computing services and office productivity software. Meanwhile, GAAP net income soared 57% to $23.7 billion, helped along by a continued focus on cost control.

Going forward, Wall Street analysts estimate that Alphabet will grow earnings per share at 17% annually over the next three to five years. That forecast makes its current valuation of 26.8 times earnings seem reasonable, despite being a premium to the three-year average of 24.6 times earnings. From that valuation, I believe Alphabet can outperform the Nasdaq Composite over the next five years, as it did over the last five.

2. CrowdStrike

CrowdStrike offers more than two dozen cybersecurity products through a single platform. The company is a market leader in endpoint security software and MDR (managed detection and response) services, but its platform addresses multiple end markets and CrowdStrike is gaining share in several of them, including cloud security, identity protection, and security information and event management (SIEM).

CEO George Kurtz attributes that success to superior artificial intelligence capabilities and unique engineering that makes its platform the “easiest and fastest cybersecurity technology to deploy.” Additionally, businesses are increasingly interested in reducing costs by consolidating on a single platform, especially one with a reputation for industry-leading threat detection like CrowdStrike’s Falcon platform.

CrowdStrike reported strong financial results in the fourth quarter. Revenue increased 33% to $845 million and non-GAAP net income jumped 102% to $0.95 per diluted share. In the press release, Kurtz said, “Customers favor our single platform approach.” He also noted that businesses are standardizing on Falcon for its cloud security, identity protection, and LogScale next-gen SIEM solutions.

Management also noted strong momentum with new products, including its IT automation software (Falcon for IT) and generative AI assistant (Charlotte AI). Falcon for IT is significant because it extends CrowdStrike’s addressable market into the security-adjacent realm of observability by addressing use cases like compliance and performance monitoring. Similarly, Charlotte AI lets the company tap demand for automation.

Going forward, CrowdStrike has several tailwinds at its back. First, cyberattacks are becoming more sophisticated. Second, many enterprises still buy more than 60 point products, and half still use legacy antivirus, which fails to detect 39% of malicious software. As a result, deploying effective cybersecurity solutions (especially platforms that consolidate products) has become an IT budget priority.

With that in mind, Wall Street expects CrowdStrike to grow revenue at 29% annually over the next five years. That consensus estimate makes its current valuation of 28 times sales look reasonable. CrowdStrike more than doubled the return of the Nasdaq Composite over the last three years, and I believe it can outperform over the next five years from its current valuation.

Should you invest $1,000 in Alphabet right now?

Before you buy stock in Alphabet, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Alphabet wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $652,342!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Trevor Jennewine has positions in Amazon and CrowdStrike. The Motley Fool has positions in and recommends Alphabet, Amazon, CrowdStrike, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

History Says the Nasdaq Could Soar: 2 Top Growth Stocks to Buy Now for the Bull Market was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel