PayPal Holdings (NASDAQ: PYPL) is struggling, and one doesn’t have to go far to find examples.

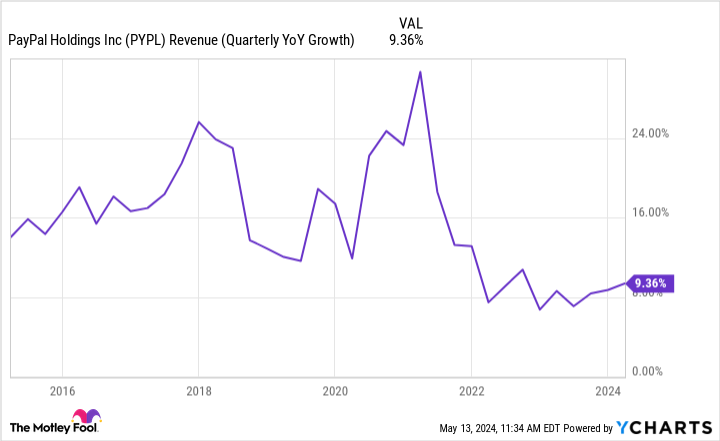

For starters, for years PayPal’s top line increased at a double-digit percentage rate. But for the past couple of years its growth rate has been much more pedestrian, with the company’s revenue only increasing by 9% in the most recent quarter.

Growth has slowed for PayPal. And here’s another struggle for the company: The growth that it does have is of lesser quality. Much of its growth has come from its unbranded checkout solution, which powers some platforms behind the scenes. This has a lower profit margin. So while its overall revenue is up, its profit has barely moved.

PayPal has struggles. But new Chief Executive Officer Alex Chriss is looking past some of them to its Venmo business, where there’s one metric that’s more than just a struggle — Chriss finds this statistic simply unacceptable.

What’s wrong with PayPal’s Venmo?

Venmo is peer-to-peer financial technology (fintech). With the mobile app, users can connect and send money back and forth, often to split the cost of a meal or similar group activity.

In the earnings call to discuss financial results for the first quarter of 2024, here’s what Chriss had to say: “There’s $18 billion of net new funds that flow into the platform of Venmo every single month. Eighty percent of those dollars leave within 10 days. That is just unacceptable.”

PayPal’s management apparently wants its users to pay for things from their Venmo accounts, not transfer balances to other financial institutions to pay from there. The inferred reason for this is that banks make easy money off of customer balances. But that’s precisely why it may be hard to persuade people to keep funds in Venmo.

First, Venmo isn’t a bank, and doesn’t come with the same guarantees that traditional bank accounts do. Second, bank accounts earn interest — not much, but at least it’s something. By contrast, money in Venmo doesn’t earn anything. In short, there’s no reason to keep a Venmo balance. In fact, it’s shocking to me that Chriss says that 20% of the money actually does sit there.

What’s the plan?

Before investing in PayPal stock, one should know what the company owns and how it fits into the bigger picture. In this case, Venmo accounts for 17% of PayPal’s total business from a payment volume perspective as of Q1. And the platform has 60 million monthly active users — not inconsequential.

Both the PayPal platform and the Venmo platform mostly address the same side of the fintech ecosystem: consumers, not businesses. I’ve noted that Chriss wants users to pay for things from Venmo, but the same could be said for PayPal’s core platform as well. To stimulate this, the company is pushing its debit card, which allows the digital-first company to process transactions offline — this is part of Chriss’s plan to deal with what he finds unacceptable for Venmo.

Growth is encouraging for both platforms in this respect. In Q1, only about 4% of PayPal’s accounts used the accompanying debit card. But first-time debit card users were up 38% year over year. Over on Venmo, there was a 21% increase in debit card users.

What now?

There are some encouraging signs with Venmo, but PayPal is facing an uphill climb to get more funds to stay on the platform instead of being transferred elsewhere. Investors should watch debit-card penetration in upcoming quarters since this is a point of emphasis from management. Increased debit card usage could lead to better monetization of Venmo.

That said, PayPal is still the dominant part of this business, and management has said that 2024 will be a “transition year.” This means that overall financial results may take time to show improvement, giving investors plenty of time to calmly evaluate PayPal’s progress with Venmo for now.

Should you invest $1,000 in PayPal right now?

Before you buy stock in PayPal, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PayPal wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $553,880!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends PayPal. The Motley Fool recommends the following options: short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

PayPal Is Struggling: Here’s What Its New CEO Finds “Unacceptable” was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel