The word “cheapest” in reference to stocks can mean many things. For example, it could indicate a stock price or its valuation. Snowflake (NYSE: SNOW) is at or near all-time lows in both of these metrics. Some may see this as a problem, as nobody wants to catch a falling knife. Others may see it as a buying opportunity, as it’s not often you can pick up shares at a discount to historical valuation levels.

So, is it time to buy Snowflake stock?

Snowflake’s stock hasn’t been great to own recently

Snowflake is a direct beneficiary of the artificial intelligence (AI) arms race. Its products center around the data cloud, a vital part of AI. Quality data makes a powerful AI model, but storing and collecting that data efficiently isn’t always easy, as the data may be in an unstructured format. However, Snowflake’s products assist with that, making it easy to store data across multiple providers and transfer it as necessary.

With Snowflake’s product in mind, it seems odd that the stock is moving in the opposite direction of nearly every other stock associated with AI, but it is down over 30% this year.

The lowest Snowflake’s stock has ever been was in mid-2022, when shares bottomed at $113. While Snowflake is still a ways off from that low, it’s never good to be approaching an all-time low, as it indicates something may be wrong with the business.

However, when you look at the growth, everything seems to be in order.

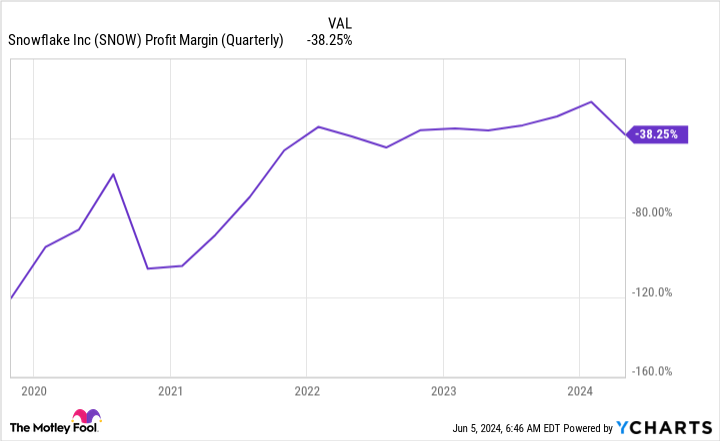

Snowflake’s financials appear to be in good shape

In the first quarter of fiscal year 2025 (ending April 30), Snowflake’s product revenue increased by 34% year over year to $790 million. Remaining performance obligations, a measure of future business on signed contracts, were up 46% to $5 billion. While this isn’t guaranteed income, when this metric outpaces revenue growth, it shows that clients are signing contracts for bigger or longer use in the future. Either way, that’s a great sign for Snowflake.

However, management’s guidance didn’t thrill investors. In the second quarter, it expects product revenue growth between 26% and 27% and fiscal year 2025 growth of just 24%. Both of these figures indicate a substantial slowdown throughout the rest of the year, which isn’t something investors want to see, especially when Snowflake is heavily involved in the AI industry.

However, investors shouldn’t read too much into those projections, as Snowflake has beaten its own expectations for multiple quarters in a row.

Quarter | Projected Product Revenue Growth | Actual Product Revenue Growth |

|---|---|---|

Q1 FY 2024 | 44.5% | 50% |

Q2 FY 2024 | 33.5% | 37% |

Q3 FY 2024 | 28.5% | 34% |

Q4 FY 2024 | 29.5% | 33% |

Q1 FY 2025 | 26.5% | 34% |

Q2 FY 2025 | 26.5% | N/A |

Data source: Snowflake.

Snowflake has consistently beaten its own projections, and I wouldn’t expect that to change in Q2.

One problem with Snowflake’s financials is how unprofitable it is. While Snowflake’s management will tell you it had a free-cash-flow (FCF) margin of 40% in Q1 (which is fantastic), this doesn’t include stock-based compensation, an expense that accounts for 43% of revenue. This causes Snowflake to be unprofitable from a generally accepted accounting principles (GAAP) basis, and it has a long way to climb before becoming profitable.

This is a bit troublesome, as Snowflake’s growth is projected to slow down (even though we can use historical trends to determine that it won’t slow down as much as management projects). When a growth stock’s revenue growth slows, it’s expected to turn profitable. Snowflake isn’t doing that, which is why many investors are concerned.

I’m not as worried, as Snowflake is still FCF positive, and many tech giants like Amazon grew to the size they are now thanks to being consistently unprofitable.

Furthermore, the stock’s price-to-sales (P/S) ratio is at its lowest level ever.

With all the momentum going against Snowflake right now, I wouldn’t be surprised if this downward trend continues as investors head for the exits. However, I think Snowflake will be a great investment over the long term, although you’ll have to be patient to realize those gains.

Snowflake is well-positioned to succeed, but it will need a blowout quarter or other positive news to turn its fortunes around.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has nearly tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now…

*Stock Advisor returns as of June 3, 2024

Keithen Drury has positions in Snowflake. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.

Snowflake Stock Is the Cheapest It Has Ever Been. Time to Buy? was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel