There are plenty of high-yield dividend stocks backed by weak businesses. There are also numerous great companies with decades of dividend increases and mediocre yields. Finding a company with a high yield and a track record of increasing its payout — now that’s an opportunity worth exploring.

When a reliable dividend stock also has a high yield, it’s typically because payouts have grown faster than the stock price. That’s exactly what has been happening with United Parcel Service (NYSE: UPS), which is down over 30% in the last three years compared to a 60% increase in the dividend.

UPS has its challenges, but the beaten-down company is too good to pass up. Here’s why.

A stagnant but attractive payout

UPS sets straightforward expectations for its dividend growth. The pecking order starts with reinvesting in the business, but after that, it’s the dividend.

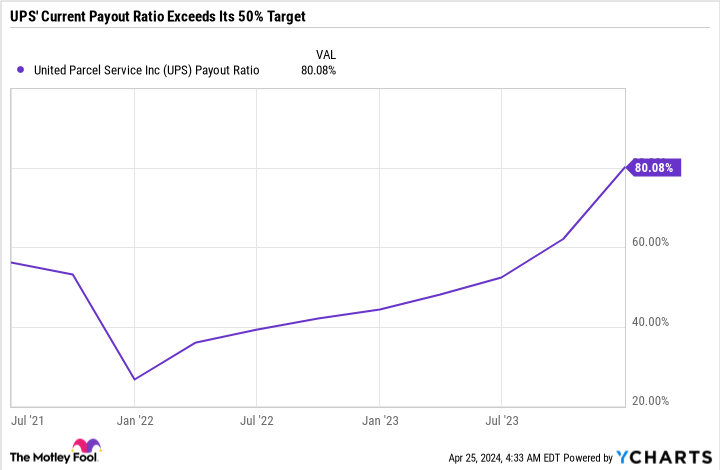

The company’s targeted payout ratio is 50% of adjusted prior-year earnings per share. However, due to declining earnings and a higher dividend, it is well beyond that target now. In the following chart, you can see the massive 49% dividend raise UPS made in early 2022 and how it impacted the payout ratio.

The good news is that UPS has no intention of cutting the dividend, choosing instead to improve the business to decrease the payout ratio. UPS CEO, Carol Tome, said the following on the Q1 2024 earnings call:

It’s our intent to earn back into a 50% payout ratio over time. We have no intent to cut the dividend to make that math work. We’re going to earn back into it and the dividend is an important part of the value proposition. So we just raised the dividend and we look to, of course, subject to board approval, we look to raise the dividend every year.

UPS has paid and raised its dividend for 15 consecutive years. The last dividend raise was a minimum one-cent per-share per-quarter increase. Judging by management’s commentary on the earnings call, I would expect minimum raises to continue until the payout ratio comes down.

Normally, minimum raises would be cause for concern. But given UPS’ downturn and the stock’s already hefty yield of 4.4%, it looks like the right move. The question now is determining if UPS has a clear roadmap for growing earnings and turning the business around to return to growth.

UPS’ three-year plan

UPS wants to be the top complex healthcare-logistics provider in the world. Healthcare revenue reached $2.6 billion in the first quarter of 2024, but the company expects healthcare revenue to be $20 billion by 2026 — roughly double what it is today.

To get there, UPS is expanding its coverage, boosting key shipping routes, and building facilities for lab customers. The healthcare segment has a higher margin because it focuses on time and temperature-sensitive shipments like lab samples. Healthcare, in general, is a more complex shipping frontier even for less time-sensitive products like medical devices and home-healthcare products.

Healthcare embodies UPS’ strategic initiative around its “better, not bigger” framework, which focuses on margin growth rather than just sales growth.

UPS forecasts moderate delivery-volume increases, just a 5.5% compound annual growth rate in U.S. small packages between 2024 and 2026. UPS believes that the growth, paired with efficiency improvements and healthcare expansion, will allow the company to reach $108 billion to $114 billion in 2026 revenue and an adjusted-operating margin of at least 13%.

At the midpoint of that guidance, UPS would earn operating income of $14.4 billion, which is more than 50% higher than its trailing-12-month (TTM) operating income of $9.1 billion. That kind of operating income makes the dividend expense look much more affordable and sets the stage for future raises. The numbers can get a little complicated since we are discussing operating income, and the payout ratio is based on net income. But we do know that UPS’ TTM dividend expense was $5.4 billion, and its net income was $6.7 billion. In other words, UPS could have a payout ratio below 50% based on its 2026 goals.

A long road ahead

UPS’ plan sounds great on paper, but it still has to execute to get there. Its 2024 guidance calls for $92 billion to $94.5 billion in revenue and an adjusted-operating margin between 10% and 10.6%, which would be $9.6 billion in operating income at the midpoint of both those ranges. It’s not a big improvement, but it’s still a step in the right direction.

The company’s investor and analyst conference from late March detailed why the ramp-up in margins should start to take shape in 2025 and 2026, so UPS has already given itself a cushion in 2024.

The best way to approach an investment in UPS is to think at least three to five years out by focusing on the company’s progress toward those 2026 goals rather than getting too caught up in the quarterly results. UPS was way too optimistic about post-pandemic package-delivery volume growth and has been hit especially hard by the industrywide downturn. However, it is making the right strategic moves to position the company for high-margin growth.

In the meantime, the 4.4% dividend yield is a compelling incentive to hold the stock and give the story time to play out. Investors looking for value, passive income, and future growth could consider buying UPS, especially with the stock hovering around a 52-week low.

Should you invest $1,000 in United Parcel Service right now?

Before you buy stock in United Parcel Service, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and United Parcel Service wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $544,015!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 30, 2024

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool recommends United Parcel Service. The Motley Fool has a disclosure policy.

This Dividend Stock Yields 4.4% and Has 15 Consecutive Years of Dividend Increases. Here’s Why It’s a Buy Now was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email news@emeatribune.com Follow our WhatsApp verified Channel