Sometimes quality companies that have fallen on hard times can make for great investments. The market usually sells off their stocks to levels more than warranted when the underlying business hits a lean patch, or fails to meet the market’s baked-in expectations, over the short term. But if the long-term prospects are fundamentally intact, such market actions merely make the stocks cheap, making them ripe pickings for value investors.

However, it’s also true that many investors have lost their shirts by betting on fallen winners from yesteryear in hopes of a recovery that never arrived.

Undoubtedly, it’s hard to distinguish which stocks are in which of the two categories above. So, let’s examine one example of each.

One to buy: Pfizer

Despite its high-profile work in developing a coronavirus vaccine at the start of the pandemic, the total return of Pfizer‘s (NYSE: PFE) shares over the last three years is down by 11%, badly underperforming the market. And it isn’t as though the company can tell shareholders that it’ll surpass its top line of $100 billion in 2022 anytime in the next few years. The windfall profits have all been realized already, and demand for its anti-coronaviral products will decline until it reaches its long-term level.

But that doesn’t mean its dividend will stop rising over time, albeit at a slow pace.

Nor does it mean that the company’s ability to pay its dividend will be threatened, and management actually plans to increase its capital allocated to shareholders as soon as it’s done paying down the debt from its recent acquisition of Seagen, a cancer therapeutics business. With $64 billion in debt and repayment at the pace of the fourth quarter, when it repaid $1.3 billion of its long-term borrowing, that project will take some time.

But with the benefit of Seagen and a few other acquisitions, the future looks bright. In total, by 2030 Pfizer is aiming to gain $45 billion in new revenue. Few other businesses can say that their next six years will see as much additional sales in absolute terms, and with a world-class management team, Pfizer is more likely to succeed with its goal than stumble.

In that context, its forward price-to-earnings (P/E) ratio of 12 looks inexpensive, presuming you’re willing to be patient.

One to avoid: Walgreens Boots Alliance

Walgreens Boots Alliance (NASDAQ: WBA) is struggling to find its home in the U.S. healthcare market. Its traditional fare, consumer-facing pharmacies, is no longer sufficient to drive growth. At the same time, its dividend was cut this year from $0.48 per quarter to $0.25, and it is unclear when its payment will return to growth.

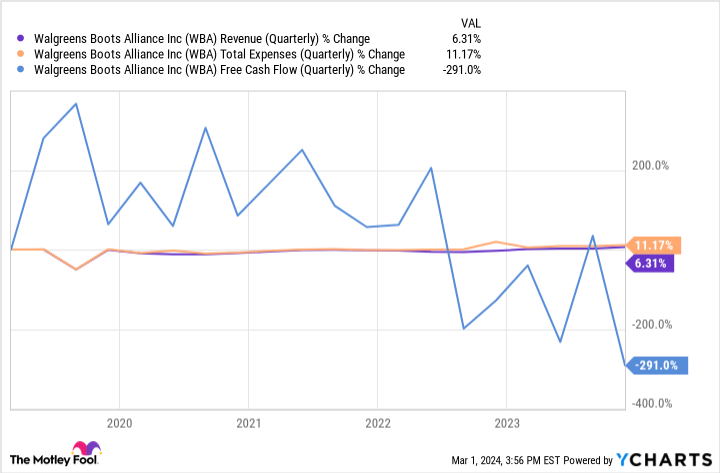

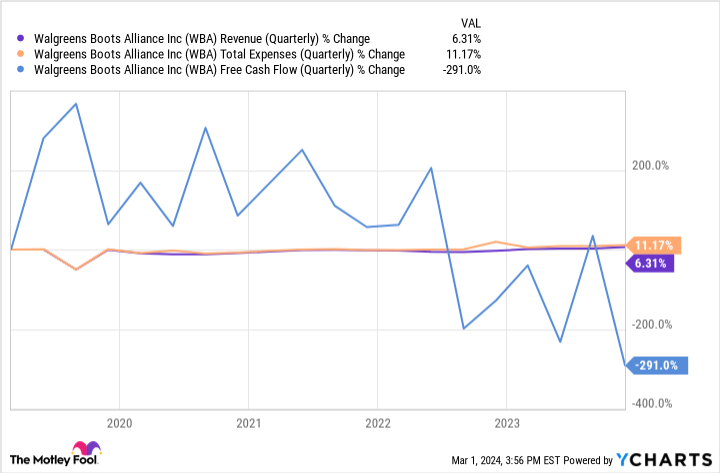

The smart move is to expect that it will take years. Despite its recent strategic entry into the primary care segment, its top line is not expanding rapidly, and its expenditures are up, causing its free cash flow (FCF) to fall significantly over time. The below chart shows Walgreen’s falling FCF trajectory over the last five years despite near constant revenue.

As you can see, costs have risen faster than revenue, which has reduced profitability. That isn’t the situation one would expect of a well-functioning business that has historically been competing primarily in a relatively stable industry like retail pharmacies.

What’s more, Walgreens Boots Alliance has no trump card to play in its hand at this point; it faces a grueling combination of slashing costs necessary to generate revenue by closing stores and the need for major new outlays to capture market share. Shareholders already paid the bill for the dilemma once when the dividend was cut, and they might need to pay for it again, too.

The company has been selling off hundreds of millions of dollars of its investments to cover its near-term costs. That will likely continue for the foreseeable future, but eventually it will run out of investments to sell. Plus, each sale decreases its assets, which is not favorable.

Worse yet, Walgreens’ leaders see 2024 featuring more headwinds than tailwinds, so don’t feel like you need to buy this stock.

Should you invest $1,000 in Pfizer right now?

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 8, 2024

Alex Carchidi has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Pfizer. The Motley Fool has a disclosure policy.

1 Bruised Dividend Stock to Buy While It’s Cheap, and 1 to Avoid was originally published by The Motley Fool

EMEA Tribune is not involved in this news article, it is taken from our partners and or from the News Agencies. Copyright and Credit go to the News Agencies, email [email protected] Follow our WhatsApp verified Channel